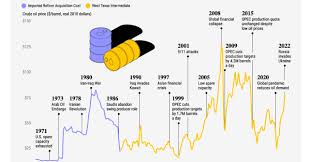

OPEC+ agreed on a gradual output increase of 548,000 barrels per day (bpd) starting August 2025, as part of a plan to phase out the voluntary cuts of 2.2 million bpd.

OPEC+ has unanimously agreed to gradually increase oil output by 548,000 barrels per day (bpd) beginning August 2025, as part of a strategic plan to phase out the voluntary production cuts totaling 2.2 million bpd implemented earlier. This decision aims to restore supply levels while balancing market stability amid ongoing uncertainties.

According to several industry experts interviewed by Argaam, this move reflects the alliance’s careful approach to supporting oil markets without triggering excessive price pressures. The experts emphasized that the decision’s inherent flexibility allows OPEC+ to adjust in response to unexpected demand fluctuations or geopolitical developments.

Oil Price Projections and Market Outlook

Analysts project that oil prices could stabilize within the range of $70 to $85 per barrel in the second half of 2025, depending on global economic conditions, demand recovery, and geopolitical developments. Factors influencing these projections include:

- Global Economic Growth: A tentative recovery is expected in major economies like China and the US, which could boost oil demand. However, uncertainties surrounding inflation, interest rate hikes, and potential recession risks remain a concern.

- Supply Dynamics: The phased increase in production may put downward pressure on prices if global demand does not keep pace, but the planned gradual approach aims to prevent sharp declines.

- Geopolitical Risks: Tensions in the Middle East, disruptions in major oil-producing regions, or strategic moves by oil exporters could influence prices upward or downward unexpectedly.

Future Outlook

While current projections favor a stabilization of prices, market analysts caution that volatility remains possible due to external shocks, changes in global energy policies, or shifts in demand patterns driven by technological advancements and climate policies. The flexibility built into OPEC+’s decision provides a crucial tool to adapt to these dynamic market conditions and ensure a balanced supply-demand equation in the upcoming months.Several experts told Argaam that the decision reflects the alliance’s attempt to strike a delicate balance between supporting market stability and avoiding price pressures, especially amid uncertainty about the global economic outlook. They stressed that the flexibility of the decision gives OPEC+ room to respond to any unexpected demand or geopolitical shocks.

Strategic flexibility and cautious expansion

Wael Makarem, Chief Market Strategist at Exness

Wael Makarem, Chief Market Strategist at Exness, said OPEC+ is likely to continue a gradual output increase during the July meeting, with strict adherence to the scheduled quantities as part of a flexible policy that allows for adjustment or temporary suspension based on market conditions. In a phone call with Argaam, Makarem explained that this flexibility gives the alliance a strategic tool to manage the market proactively, especially in light of the economic uncertainty stemming from rapid shifts in US trade policies.

Ali Al-Riyami, former Director General of Oil and Gas Marketing at Oman’s Ministry of Energy and Minerals

For his part, Ali Al-Riyami, former Director General of Oil and Gas Marketing at Oman’s Ministry of Energy and Minerals, said that the eight OPEC+ countries will continue injecting around 411,000 bpd from August through October 2025, as part of a plan to gradually restore the withheld volumes through the end of 2027 He noted in a call with Argaam that the timing of the increase is appropriate, especially with the rising demand during the summer season, which coincides with peak travel. He added that the decision had limited impact on prices over the past three months due to overlapping political and trade factors, most notably geopolitical tensions, ambiguity around tariffs, and the unclear global economic outlook.

He confirmed that these factors contributed to a timely OPEC decision, starting with the implementation of the increase in May. However, he warned that the fourth quarter of 2025 may reveal real challenges, questioning whether Chinese growth will be sustainable or temporary, which has a direct impact on market trends. Regarding seasonal gasoline demand in the US, Al-Riyami explained that the observed decline is linked to weekly data fluctuations and storage conditions.

However, he pointed out that global demand levels remain stable between 104 and 105 million bpd, according to OPEC and IEA reports, confirming that the shift toward renewable energy has yet to make a tangible impact on actual oil consumption.

Global demand: China and the US in focus

Makarem noted that developments in the Chinese economy significantly affect global oil demand expectations, as China is one of the largest sources of demand. He pointed out that the slowdown in the services sector, which reached its lowest level in several months, could lead to weaker transportation fuel consumption and thus impact overall demand forecasts. He added that the rise in US inventories reflects a relative decline in consumer demand, adding pressure on market stability. Meanwhile, Al-Riyami said economic activity in China remains stable at acceptable levels, especially after government intervention at the end of Q4 2024 to support the industrial, real estate, and commercial sectors, which helped stabilize growth.

He added that any effective trade deal between China and the US —despite the lack of full details—would stabilize China’s economy and increase commercial activity in 2026, thereby gradually boosting oil demand, albeit modestly. He emphasized that the relationship between Beijing and Washington, particularly regarding tariffs, is a critical factor in shaping oil demand patterns.

Concerns over excess supply of crude oil in the near-term have put spot prices under pressure in the recent past. Graphic: Mint

Spot Brent crude prices closed below $70 a barrel on Friday. For the last one week, Brent crude prices have moved into what the markets call contango, a phenomenon where the spot price is lower than that of a futures contract. The chart above has the details.

Contango indicates that the markets are concerned about oversupply at the moment. The recent fall in oil prices was triggered because the US granted waivers to eight countries to continue importing crude oil from Iran (including India and China, top buyers of Iranian crude oil) for 180 days. The markets are relieved that Iranian crude oil supply in the global markets will not drop sharply in the near term, even as the exact quantum is not clear.

In general, the risk-off sentiment in the markets (seen in October) and an environment where interest rates are rising have also cast its shadow on crude oil prices. Additionally, there have been concerns on the demand outlook.

Moving ahead, the million-dollar question is the direction that crude oil prices will take. According to Ashray Ohri of ICICI Bank Ltd, “While a further fall may be warranted based on US’s temporary exemption on Iran and demand concerns, we believe oil prices are more likely to move to the upside as Iran exports get depleted further.”

Having said that, is $80 a barrel on the horizon?

“We believe a Brent rebound above the $80 a barrel level is less likely based on the current fundamentals and more responsible statements made by the US administration,” wrote Ohri in a report on 6 November. “As such, we expect oil prices to trade around the $75 a barrel mark and average $77 a barrel in the fourth quarter of this year, before cooling further to average $75 a barrel in Q1 2019.”

Of course, much also depends on the stance that the Organization of the Petroleum Exporting Countries and its friends take on production cuts.

For now, lower crude oil prices are good news for us, as India imports a huge portion of its oil requirements. Lower prices benefit the country’s current account deficit and ease pressure on the rupee. For many corporates too, easing crude oil prices will bring some relief on the costs front.

OPEC+ decisions: Navigating economic and geopolitical factors

According to Makarem, OPEC+ decisions are based on global demand forecasts, which are linked to economic growth, aiming to avoid oversupply and ensure price stability.

He explained that maintaining appropriate prices is essential to cover member states’ budget needs, and that preserving market share is a strategic objective.

Meanwhile, Al-Riyami noted that geopolitical factors play a role no less important than economic ones in shaping OPEC+ decisions.

He confirmed that the market has gradually adapted to the recent production increase and that the summer supply-demand balance supports continued current output levels.

Al-Riyami warned that large oil inventories in major countries could reshape the market later, considering Q4 2025 and Q1 2026 to be pivotal for OPEC+ strategies.

He also expects the current policy to continue without further voluntary cuts, likely adjusting based on market and geopolitical developments, especially those related to global trade.

He pointed out that improved trade conditions—particularly those related to tariffs between China and countries like India, Japan, Canada, and Europe—would support the global economy and reflect positively on oil demand.

He expressed optimism about the possibility of reaching trade agreements and easing geopolitical tensions, especially in the Gulf and the Middle East, stressing that the world needs a period of stability, given its direct impact on people’s daily lives and global markets.